The UPI Trap: Are You Making This Common Mistake? A Guide to Secure Digital Payments

The UPI Trap: Are You Making This Common Mistake? A Guide to Secure Digital Payments

The Unified Payments Interface (UPI) has revolutionized how India transacts, making payments as simple as a few taps on a smartphone. While its convenience is unmatched, its simplicity has also become a breeding ground for scams. One specific mistake, committed by millions of users daily, makes them an easy target for fraudsters. Are you making this common, yet dangerous, error?

The One Mistake That Puts You at Risk

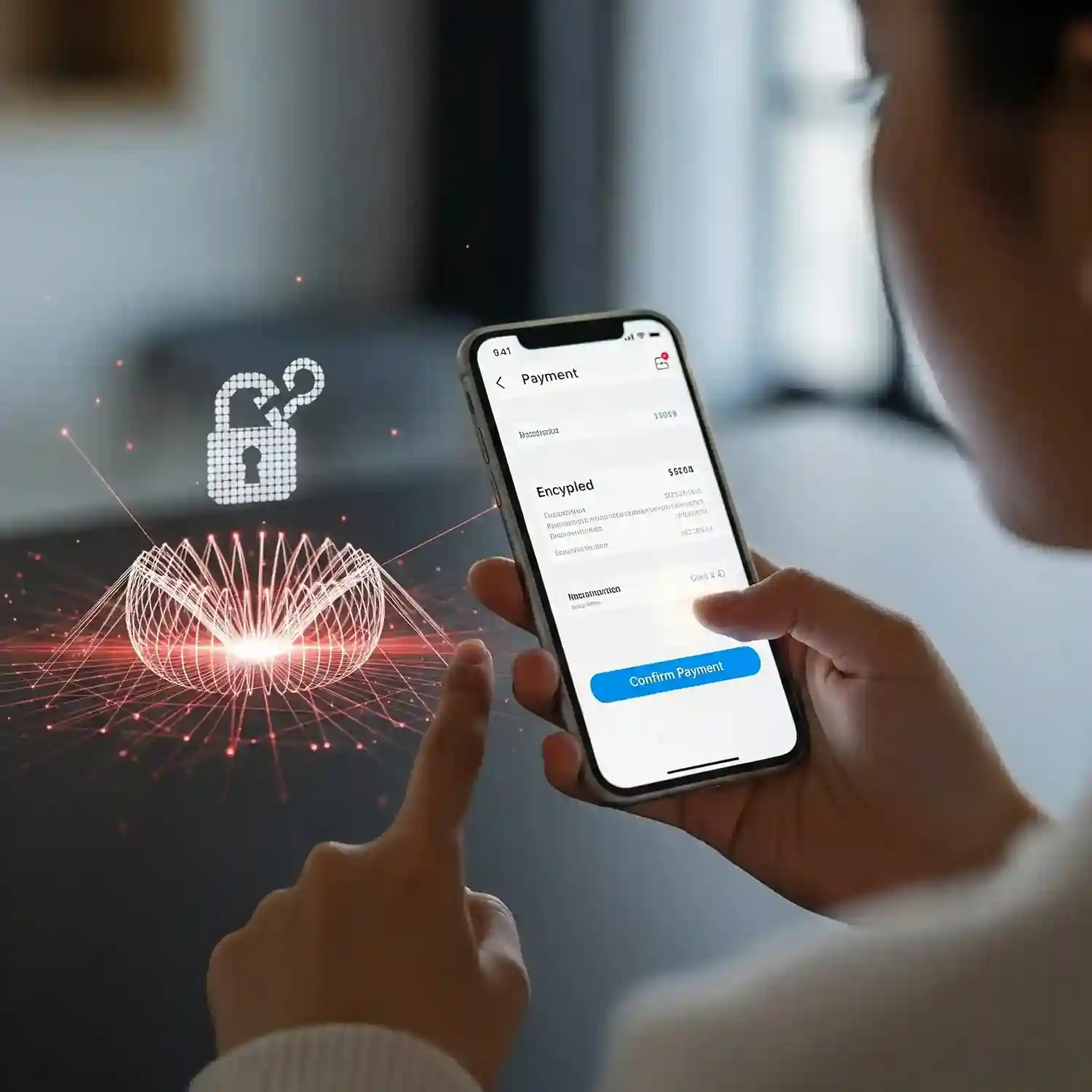

The most common trap in the world of UPI is the belief that you need to enter your UPI PIN to receive money. This is a critical and dangerous misunderstanding. Your UPI PIN is only required for two actions:

- To send money to someone.

- To approve a debit from your account (e.g., for a QR code payment or a merchant transaction).

A fraudster will call or message you, often pretending to be from a government agency or a company, and claim they need your UPI PIN to "process a refund" or "deposit funds." When you enter your PIN on their instruction, you are not receiving money; you are authorizing a payment from your own account.

How to Stay Safe: Simple Rules to Live By

- Never Share Your PIN: This is the golden rule. No one, not your bank, not a customer service agent, and certainly not someone sending you money, needs your PIN. The UPI system is designed for a recipient to receive money without any action other than providing their UPI ID or QR code.

- Be Wary of "Request Money" Scams: Scammers can send you a "Request Money" alert with a fake message like "Your refund is ready. Approve the request to receive it." Approving this request will debit money from your account, not credit it. Always read the notification carefully to understand if it's a request to pay or a notification of a payment received.

- Set a Transaction Limit: Most UPI apps allow you to set daily transaction limits. Set a low limit to ensure that even if you fall for a scam, the financial damage is minimal.

- Use Biometric Security: Enable fingerprint or face ID authentication on your UPI app for an extra layer of security.

By understanding this simple distinction—that a UPI PIN is for paying, not receiving—you can protect yourself and your loved ones from a majority of digital payment frauds.